Accounting is the language of business, but for newcomers, accouting terms and processes can feel like a maze. Why is it so important? Accurate records influence every decision and keep you on track for success.

This guide cuts through the confusion, giving you the essential knowledge and step-by-step strategies to master your finances in 2025. You'll discover the basics, key principles, practical setup steps, must-have tools, common mistakes to avoid, and top resources for ongoing learning.

Ready to get started? Let’s demystify accouting together and build your roadmap to financial confidence.

Understanding Accounting Basics

Starting your accouting journey can feel intimidating, but understanding the basics is the first step to financial confidence. Whether you’re launching a business or managing personal finances, a strong foundation in accouting helps you make smarter, data-driven decisions. Let’s break down the essentials so you can see how accouting serves as the backbone of every successful venture.

What is Accounting and Why is it Important?

Accouting is the systematic process of recording, summarizing, and analyzing financial transactions. It’s not just about crunching numbers; accouting provides a clear picture of where your money comes from and where it goes.

For businesses, accouting is crucial for tracking cash flow, planning budgets, and making informed decisions. Even on a personal level, accouting helps you stick to financial goals and avoid overspending. Consider this: a U.S. Bank study found that 82% of businesses fail due to poor cash flow management—highlighting the real-world impact of sound accouting practices.

Accouting also ensures you meet legal and tax obligations. Accurate records support compliance, reduce audit risks, and make tax filing much smoother.

Core Accounting Principles and Concepts

Every accouting system is built on foundational rules known as Generally Accepted Accounting Principles (GAAP). These principles ensure consistency and transparency in financial reporting.

One of the first choices is between the accrual and cash basis methods. The accrual method records transactions when they occur, while the cash basis records them when money changes hands. If you want a deeper dive, check out this comprehensive Accrual vs. Cash Basis Accounting guide.

Double-entry bookkeeping is another core concept—every transaction affects at least two accounts, keeping the books balanced. The matching principle ensures expenses are recorded in the same period as related revenues, while revenue recognition dictates when income is officially counted. For example, selling a service today but receiving payment next month is handled differently depending on your accouting method.

Types of Accounting: Financial, Managerial, and Tax

Accouting isn’t one-size-fits-all. There are three primary types to know:

Financial accounting focuses on preparing reports for external stakeholders—think income statements for investors.

Managerial accounting is for internal decision-making, helping managers plan, budget, and set goals.

Tax accounting ensures compliance with government regulations and helps with tax planning.

For instance, a retail store uses financial accouting to report profits, managerial accouting to control inventory, and tax accouting to file returns. Understanding these distinctions in accouting empowers beginners to choose the right focus for their needs.

Key Accounting Terminology for Beginners

To speak the language of accouting, you need to know its essential terms:

Assets: What you own (cash, equipment)

Liabilities: What you owe (loans, bills)

Equity: Owner’s share after liabilities

Revenue: Money earned from sales

Expenses: Costs of running the business

Profit: What’s left after expenses

The heart of accouting is the accounting equation: Assets = Liabilities + Equity

Mastering these terms helps you understand reports and communicate clearly with accountants or stakeholders. A solid grasp of accouting vocabulary is the foundation of financial literacy.

The Accounting Cycle: Step-by-Step Overview

Accouting follows a structured cycle to ensure accuracy and completeness. The steps include:

Recording transactions as they happen

Creating journal entries for each transaction

Posting entries to the ledger

Preparing a trial balance to check for errors

Making any necessary adjustments

Producing financial statements

Closing the books for the period

Each step builds on the previous one, forming a complete picture of your finances. For example, buying office supplies starts with a receipt, is recorded in the journal, posted to the ledger, and ultimately appears in your financial statements. Understanding this accouting cycle ensures nothing slips through the cracks.

Setting Up Your Accounting System

Getting your accouting system up and running is a crucial step for any beginner. A solid foundation ensures you keep accurate records, stay compliant, and make smart business decisions. Let’s walk through each step to help you build a system that fits your needs and sets you up for success.

Choosing the Right Accounting Method

The first decision in accouting is selecting between the cash and accrual methods. Cash accounting records transactions when money changes hands, making it simple and easy for many freelancers and small businesses. Accrual accounting, on the other hand, records income and expenses when they’re earned or incurred, giving a more accurate picture of your financial health.

Consider your business type and legal requirements. Service-based businesses often prefer cash accounting for its simplicity, while retail or inventory-heavy businesses may benefit from the accrual method. For a detailed comparison, see Cash vs. Accrual Accounting Differences.

Choosing the right method shapes how you handle accouting tasks, so review your options carefully before you begin.

Selecting Accounting Software and Tools

Modern accouting software streamlines your workflow and reduces manual errors. Popular options include QuickBooks, Xero, and FreshBooks, each offering unique features for different needs. You’ll want to consider whether a cloud-based or desktop solution fits your workflow and budget.

Here’s a quick comparison to help you decide:

Software

Cloud/Desktop

Key Features

Best For

QuickBooks

Both

Invoicing, Reporting

Small Businesses

Xero

Cloud

Integrations, Automation

Growing Companies

FreshBooks

Cloud

Simple Expenses, Invoices

Freelancers

Over 64% of small businesses use accouting software for its efficiency and scalability. Choose a tool that can grow with your business and integrates with your other systems.

Creating a Chart of Accounts

Your chart of accounts is the backbone of your accouting system. It organizes every transaction into categories like assets, liabilities, revenue, and expenses. Most systems use a numbering scheme to keep things tidy and easy to track.

A basic chart for a small business might look like this:

Customize your chart to fit your business or personal accouting needs. A clear structure from the start saves time and confusion down the road.

Setting Up Record-Keeping Processes

Organized record-keeping is essential for accouting accuracy and legal compliance. You’ll need to decide between digital and paper records—digital is often more secure and easier to search, but requires good backup practices.

Tips for effective record-keeping:

Use folders for receipts, invoices, and tax documents.

Set a monthly checklist to review and file documents.

Secure sensitive data with strong passwords and encryption.

Developing these habits early makes accouting less stressful and more reliable, especially during tax season.

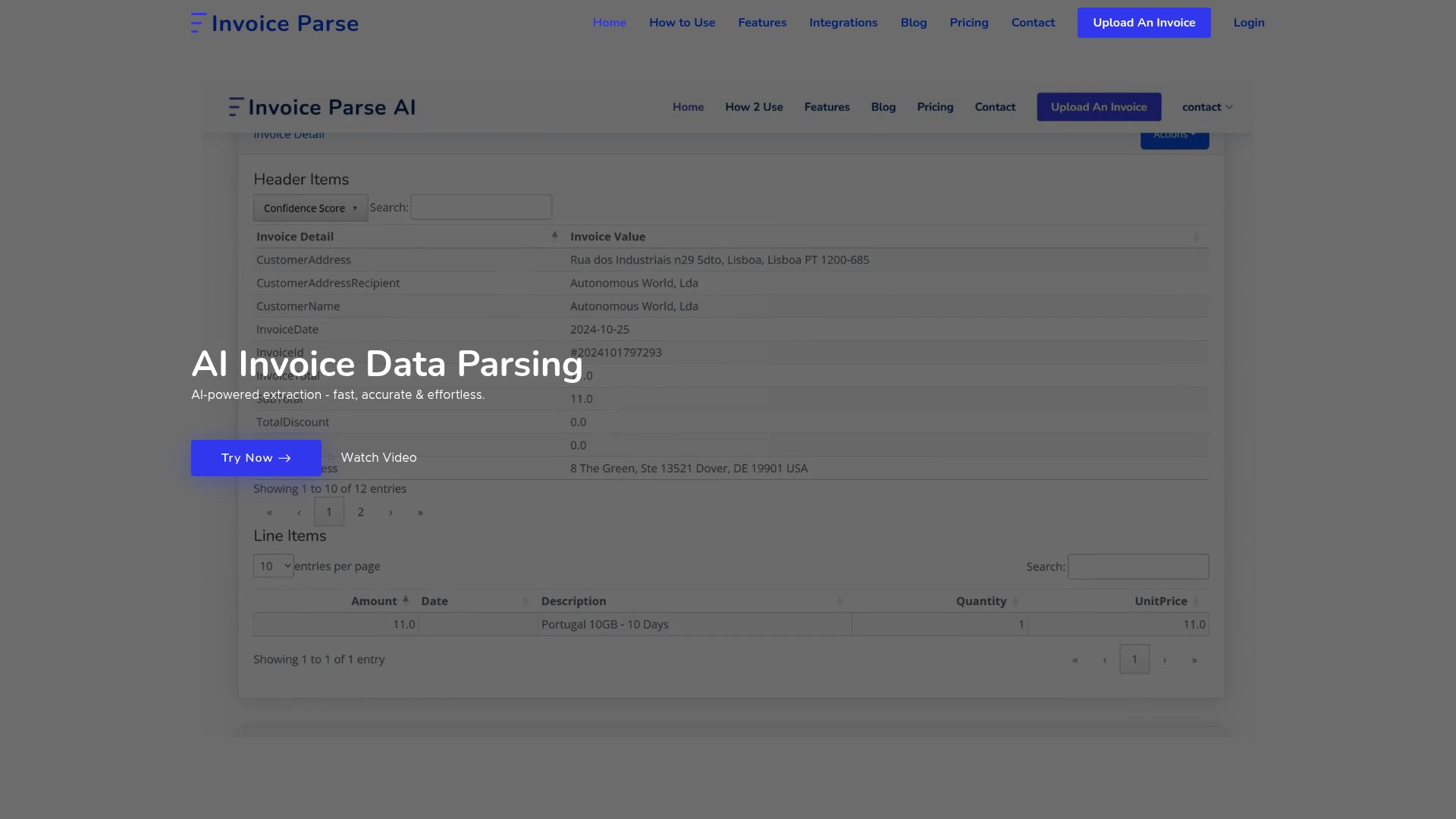

Integrating Automation and AI in Accounting

Automation is transforming accouting for beginners and professionals alike. Automated bank feeds, receipt scanning, and invoice parsing can save hours each month and reduce errors from manual entry.

AI-powered analytics are becoming commonplace, helping businesses spot trends and forecast finances. For example, you might automate expense categorization or integrate your accouting software with your bank for real-time updates.

Embracing automation means you spend less time on repetitive tasks and more time making informed decisions.

Manual data entry is one of the most tedious accouting tasks for beginners. AI tools like Invoice Parse use smart algorithms to extract key details from invoices, even if you don’t have a template. This means you can upload a PDF or scan, and the tool pulls out the vendor, amounts, and dates automatically.

Benefits include faster processing, greater accuracy, and seamless integration with platforms like Excel or Power BI. Imagine a freelancer uploading a stack of invoices and having all the data ready for accouting analysis in minutes.

By leveraging AI, you simplify your workflow and reduce the risk of costly errors.

Essential Accounting Tasks for Beginners

Whether you’re just starting your accouting journey or looking to sharpen your skills, mastering essential tasks is the foundation for confident financial management. Each task builds on the last, making your accouting process smoother and more reliable over time.

Recording Transactions Accurately

Accurate transaction recording is the heartbeat of accouting. Every sale, purchase, or expense must be logged promptly to keep your records reliable.

Start by collecting all supporting documents, like invoices or receipts. Enter each transaction into your chosen accouting system, making sure to note the date, amount, and category.

A simple business expense entry might look like this:

Date: 2025-01-10

Account: Office Supplies

Amount: $45.00

Description: Printer paper and pens

Double-check entries for typos or missing details.

Regularly review for errors to catch issues early.

Use consistent categories to simplify reporting.

By making transaction recording a daily habit, you’ll avoid confusion and keep your accouting records audit-ready.

Managing Accounts Payable and Receivable

Accouting isn’t just about tracking what you spend—it’s also about monitoring what you owe (accounts payable, AP) and what you’re owed (accounts receivable, AR). Keeping these organized ensures healthy cash flow.

Start by listing all outstanding bills and invoices. Create an aging report to monitor overdue amounts. Set reminders for upcoming payments and follow up with clients on unpaid invoices.

Mastering AP and AR management helps your accouting system reflect your true financial position.

Reconciling Bank Statements

Reconciling your bank statements is a crucial accouting task that prevents errors and detects fraud. Each month, compare your accouting records with your bank statement.

Here’s a step-by-step process:

Collect your latest bank statement and accouting ledger.

Match each transaction, marking off those that appear in both.

Investigate discrepancies or missing entries.

Adjust your records as needed.

Templates or accouting software can simplify this process, highlighting unmatched items automatically.

Regular reconciliation protects your business from costly mistakes and keeps your accouting accurate for decision-making.

Preparing Basic Financial Statements

Financial statements are the scorecards of your accouting efforts. The three essentials are:

Statement

What It Shows

Example

Income Statement

Profit or loss over time

Revenue - Expenses = Net Income

Balance Sheet

Financial position at a point

Assets = Liabilities + Equity

Cash Flow Statement

Cash in and out over a period

Operating, Investing, Financing flows

Prepare these by summarizing your accouting records monthly or quarterly.

Review for accuracy before sharing.

Use them to spot trends and guide decisions.

Share with stakeholders as needed.

Understanding these statements unlocks the true value of your accouting data.

Budgeting and Forecasting

Budgeting is the forward-looking side of accouting. Start by listing expected income and routine expenses for the month.

Steps to build a simple budget:

Gather past accouting data.

Estimate income for the period.

List regular and variable expenses.

Set spending limits in each category.

Forecasting uses this historical data to predict future trends, helping you plan for growth or lean times.

For example, a freelancer might budget $2,000 for expenses and forecast $4,000 in income, adjusting as actual numbers come in.

Effective budgeting guides your accouting decisions and keeps you financially prepared.

Ensuring Regulatory Compliance and Tax Readiness

Staying compliant is a must in accouting. Know your tax deadlines and required forms, such as 1099s or quarterly estimated payments.

Best practices include:

Keep digital copies of all receipts.

Update your accouting records regularly.

Set reminders for filing dates.

As tax season approaches, review your accouting data to ensure nothing is missing. If you’re a sole proprietor, organize expenses by category to speed up filing.

Reliable accouting practices make compliance less stressful and help you avoid penalties.

Common Accounting Mistakes and How to Avoid Them

Even the most diligent beginners can slip up with accouting. Recognizing common pitfalls early is your best defense. Let’s explore the top mistakes new accouting practitioners make—and how to sidestep them.

Misclassifying Expenses and Income

Mixing up business and personal expenses is a classic accouting blunder. This mistake can distort your financial statements and create tax headaches. For example, recording a personal dinner as a business meal falsely inflates your deductible expenses.

To avoid this, always use separate accounts for business and personal transactions. Take time to review Understanding Basic Accounting Terms to master key concepts and categories. When unsure, consult your chart of accounts or seek professional advice.

Accurate categorization ensures you stay compliant and make smarter business decisions.

Failing to Reconcile Regularly

Skipping reconciliations is a risky accouting habit. Without regular checks, errors and fraud can go unnoticed, and missing transactions may pile up. Imagine discovering a bank fee months later—after it’s already drained your cash flow.

Set a monthly schedule to reconcile all bank and credit card statements. Use software features or templates to streamline the process. Reconciliation not only catches mistakes but also builds financial confidence.

Stay vigilant, and make bank reconciliation a non-negotiable part of your accouting routine.

Neglecting Backup and Data Security

Forgetting to back up your accouting data can lead to disaster. If your files are lost to a computer crash or cyberattack, recovery might be impossible. Did you know that 60% of small businesses fold within six months of a major cyber incident?

Protect yourself by enabling automatic cloud backups. Use strong passwords and consider encryption for sensitive files. Regularly test your backups to ensure you can restore data if needed.

Secure, backed-up accouting records are your safety net against unexpected data loss.

Overlooking Small Transactions

Small, everyday transactions may seem trivial, but in accouting, they add up fast. Ignoring petty cash or minor expenses can snowball into major discrepancies over time. For instance, a few missed coffee receipts each month can throw off your year-end totals.

Track every transaction, no matter the size. Use digital tools to snap and store receipts instantly. Set aside time each week to review and log small purchases.

Every detail counts—precision in accouting starts with the little things.

Not Seeking Professional Help When Needed

Trying to handle complex accouting issues solo can backfire. Payroll, taxes, and audits require specialized knowledge. Waiting too long to ask for help might result in costly errors or penalties.

Recognize your limits and don’t hesitate to consult an accountant or bookkeeper when situations get tricky. Their expertise can save you time, money, and stress.

Remember: smart accouting includes knowing when to call in a pro.

Resources and Next Steps for Accounting Mastery

Ready to take your accouting skills to the next level? Mastery comes not just from understanding the basics, but from leveraging the right resources and building strong habits. This section guides you through top books, courses, communities, tools, trends, and practical steps to keep your accouting journey on track.

Recommended Books and Online Courses

Building a solid accouting foundation starts with the right educational resources. For books, “Accounting Made Simple” by Mike Piper is a concise, beginner-friendly choice that breaks down complex topics. If you prefer hands-on learning, online platforms like Coursera, Udemy, and LinkedIn Learning offer courses tailored to newcomers.

When selecting resources, look for clear explanations, practical exercises, and updated content reflecting current accouting standards. Many courses include quizzes and case studies to reinforce learning. Don’t forget to check reviews and preview course content before enrolling.

Exploring both books and online courses ensures you grasp accouting concepts from multiple perspectives.

Useful Accounting Blogs, Forums, and Communities

Continuous learning is key in accouting, and engaging with online communities keeps you updated and motivated. Top blogs like AccountingCoach offer bite-sized tutorials and real-world examples. For peer support, Reddit’s r/accounting and the AAT forums are active spaces to ask questions and share experiences.

Participating in forums helps clarify doubts, while reading expert blogs exposes you to practical tips and industry news. Many accouting communities host AMAs or webinars where professionals answer beginner questions.

Joining these platforms accelerates your accouting growth and helps you stay connected with the latest trends.

Tools and Templates for Beginners

Getting started with accouting is easier when you use the right tools. Free templates for budgeting, invoicing, and bank reconciliation are available from sites like Microsoft Office and Google Sheets. These templates simplify routine tasks and reduce errors.

Compare using spreadsheet tools versus dedicated software. Spreadsheets are flexible for simple needs, while software like QuickBooks or Xero offers automation and reporting. As your accouting needs grow, consider scalable solutions.

Download templates that match your workflow, and customize them to fit your business or personal finances. This approach streamlines your accouting tasks and saves valuable time.

Tool Type

Example

Best For

Spreadsheet

Google Sheets

Simple tracking

Software

QuickBooks, Xero

Automation, reporting

Templates

MS Office

Invoicing, budgeting

Staying Updated with Accounting Trends in 2025

The accouting landscape is evolving fast, with automation, remote work, and ESG reporting shaping the future. Staying current ensures you remain competitive and compliant. Subscribe to newsletters, attend webinars, and follow industry leaders for the latest updates.

Make it a habit to set aside time each month to review new accouting trends. Being proactive keeps your knowledge and skills up to date.

Building Good Accounting Habits

Success in accouting comes from consistency. Establish daily, weekly, and monthly routines to review transactions, reconcile statements, and back up data. Use digital calendars or apps to set reminders for important accouting tasks.

A weekly checklist might include reviewing income, updating expenses, and reconciling your bank account. Monthly, prepare financial statements and check for errors. Building these habits early prevents small mistakes from accumulating.

Over time, these routines make accouting second nature, giving you confidence and peace of mind.

Sample Weekly Accouting Checklist:

Review all new transactions

Update receipts and invoices

Reconcile bank statement

Check outstanding payments

Preparing for Advanced Accounting Topics

Once you’re comfortable with accouting basics, consider exploring advanced areas like payroll, inventory management, and financial analysis. These topics become relevant as your business grows or your responsibilities expand.

Start by identifying which advanced topics align with your goals. For example, if you’re hiring, learn about payroll processing. If you manage stock, delve into inventory accounting. Follow a structured learning path, building on your foundational accouting knowledge.

Continuous learning ensures you’re prepared for new challenges and opportunities in accouting.

Frequently Asked Questions for Beginners

New to accouting? Here are answers to questions beginners often ask:

Q: What’s the difference between cash and accrual accouting? A: Cash accouting records transactions when money changes hands, while accrual accouting tracks income and expenses when earned or incurred.

Q: Do I need software to manage my accounts? A: Not always, but accouting software automates tasks and reduces errors.

Q: Is accouting only for businesses? A: No, personal accouting helps individuals manage budgets and taxes.

If you’re unsure, consult reliable resources or seek professional advice to strengthen your accouting journey.

Now that you’ve got a handle on accounting basics and the tools that make everything easier, why not put what you’ve learned into practice? If you’re ready to speed up your workflow and say goodbye to tedious manual data entry, give AI-powered invoice extraction a try. It’s perfect for beginners and small businesses looking to save time and avoid errors—especially when you need clean data for Excel or Power BI. You can test it out yourself with the Free Invoice Parser and see just how much simpler your accounting setup can be.