Tax season creeps up fast, and staying organized can make all the difference between smooth sailing and last-minute panic. Surprisingly, almost 20 percent of Americans file their taxes in the final week before the deadline every year. Most people think gathering paperwork is just a hassle, but it actually hides a chance to reduce stress, spot missed deductions, and maybe even increase your refund if you know where to look.

Preparing for Tax Season: A Step-by-Step Guide

Table of Contents

- Step 1: Organize Financial Documents And Records

- Step 2: Identify Applicable Tax Deductions And Credits

- Step 3: Review Last Year’s Tax Return For Accuracy

- Step 4: Consult With A Tax Professional Or Accountant

- Step 5: Prepare And File Your Tax Forms

- Step 6: Verify Submission And Confirm Receipt

Quick Summary

| Key Point | Explanation |

|---|---|

| 1. Organize your financial documents thoroughly | Create a dedicated workspace and systematically gather all necessary tax forms and records to ease the filing process. |

| 2. Identify all eligible tax deductions and credits | Analyze your financial situation to uncover specific tax benefits based on life changes, education, or employment. |

| 3. Review last year’s tax return carefully | Examine previous returns to catch patterns, errors, and opportunities that affect your current tax preparation. |

| 4. Consult a tax professional if needed | Seek guidance from a qualified accountant to optimize your tax strategy and clarify complex financial situations. |

| 5. Verify submission and obtain proof of filing | Confirm successful filing with the tax authority to ensure your return is processed and track its status promptly. |

Step 1: Organize Financial Documents and Records

Preparing for tax season starts with a comprehensive organization of your financial documents. This critical first step establishes the foundation for a smooth and accurate tax filing process. Gathering and systematically arranging your financial records will save you significant time, reduce stress, and minimize potential errors when you submit your tax return.

Begin by creating a dedicated workspace for your tax preparation. This area should be clean, well-lit, and free from distractions. Select a sturdy file box or invest in a filing cabinet with clearly labeled folders specifically for tax documentation. Critical documents you must collect include:

- W-2 forms from all employers

- 1099 forms for independent contractor work

- Investment income statements

- Receipts for deductible expenses

- Previous year’s tax return

Sort these documents chronologically and by type. Digital copies provide an excellent backup, so consider scanning paper documents and storing them securely in cloud storage or an encrypted external hard drive. Many financial institutions and employers now offer digital versions of tax documents, which can be downloaded directly from their websites, simplifying the collection process.

Pay special attention to income documentation. Compile all sources of income, including your primary job, freelance work, investment earnings, rental income, and any side gigs. Ensure you have corresponding documentation for each income stream. This thorough approach helps prevent potential discrepancies that could trigger an audit or delay your tax processing.

For self-employed individuals or those with complex financial situations, creating a comprehensive spreadsheet tracking income and expenses can be immensely helpful. This document serves as a preliminary worksheet that will streamline your tax preparation and potentially reveal additional deductions you might have overlooked.

Finally, verify the completeness of your documentation. Cross-reference your collected documents against a checklist to confirm you haven’t missed any critical paperwork.

Below is a checklist table to help you verify that all essential financial documents are organized and gathered before you begin tax preparation.

| Document Type | Example Documents | Purpose |

|---|---|---|

| Income Statements | W-2s, 1099s | Report all earned income and ensure accuracy |

| Investment Records | Dividend, interest statements | Document investment earnings and capital gains |

| Deductible Expense Receipts | Medical bills, charity receipts | Support claims for tax deductions |

| Previous Year’s Tax Return | Last year’s 1040 | Reference for income, deductions, and carryovers |

| Rental or Freelance Income | Rental agreements, 1099-MISC | Report side or independent income |

| Retirement Contributions | 401(k), IRA statements | Support for income-based tax deductions |

| Tax-related Correspondence | IRS/state letters | Ensure resolution of previous notices |

Step 2: Identify Applicable Tax Deductions and Credits

Reducing your tax liability requires strategic identification of deductions and credits that can significantly lower your overall tax burden. This crucial step transforms tax preparation from a simple documentation exercise into a proactive financial planning opportunity. Understanding the nuanced world of tax benefits demands careful attention and a systematic approach.

Start by examining your life circumstances from the past year. Major life events such as marriage, having children, purchasing a home, or pursuing higher education often unlock specific tax advantages. Homeowners, for instance, can deduct mortgage interest and property taxes, while students might qualify for education credits that directly reduce tax owed.

Tax deductions and credits fall into several key categories that require thorough investigation. Income-based deductions include contributions to retirement accounts like 401(k) and traditional IRA, which can lower your taxable income. Self-employed individuals have additional opportunities, such as deducting home office expenses, business equipment, and professional development costs.

Personal circumstances dramatically influence available tax benefits. Parents might claim child tax credits, while individuals with significant medical expenses could itemize healthcare costs that exceed a specific percentage of their adjusted gross income. Charitable donations also present potential tax advantages, provided you maintain proper documentation and adhere to IRS guidelines.

As recommended by USA.gov tax resources, carefully review all potential credits and deductions before finalizing your tax return. Consider using tax preparation software or consulting a professional tax advisor who can help identify credits you might have overlooked. Some often missed opportunities include:

- Earned Income Tax Credit

- Lifetime Learning Credit

- Retirement Savings Contributions Credit

- State and local sales tax deductions

Verify your findings by cross-referencing IRS publications and consulting multiple sources. Create a detailed worksheet listing each potential deduction or credit, including the documentation required to support your claim.

This table summarizes common tax deductions and credits identified in the article, along with the qualifying circumstances and required documentation to claim each benefit.

| Deduction or Credit | Qualifying Circumstances | Required Documentation |

|---|---|---|

| Mortgage Interest & Property Tax | Homeownership | Mortgage statements, tax bills |

| Education Credits (e.g., Lifetime) | Tuition or qualifying educational expenses | Tuition payment statements (1098-T) |

| Earned Income Tax Credit | Low-to-moderate earned income | Income documentation, dependents |

| Child Tax Credit | Having dependent children | Social Security numbers, birth certificates |

| Medical Expense Deduction | Significant unreimbursed expenses | Receipts, bills, canceled checks |

| Retirement Savings Contributions Credit | Contributions to retirement accounts | 401(k), IRA statements |

| Charitable Contributions | Donated to recognized charities | Donation receipts, bank records |

Step 3: Review Last Year’s Tax Return for Accuracy

Reviewing your previous year’s tax return is a critical step in preparing for the current tax season. This process serves as a strategic roadmap, helping you identify patterns, potential errors, and opportunities for improved financial documentation. By carefully examining your prior return, you create a comprehensive reference point that can streamline your current tax preparation.

Start by retrieving a complete copy of your most recent tax return, including all supporting schedules and forms. Digital copies stored in secure cloud storage or physical files in your tax documentation folder are ideal. Lay out the return in a clear, well-lit workspace where you can methodically review each section without distractions.

Compare your previous year’s income sources against current documentation. Pay close attention to any significant changes in employment, investment income, or personal circumstances that might impact your tax filing. Discrepancies between your remembered income and documented sources can signal potential reporting issues or missed deductions.

According to U.S. Treasury recommendations, examining your previous return helps identify common errors and potential areas of improvement. Look specifically for recurring items such as:

- Consistent reporting of investment income

- Accuracy of dependent information

- Proper calculation of deductions

- Consistency in reported business expenses

Pay special attention to any notes or explanations from previous tax preparers or software. These annotations might reveal complex financial situations or unique filing circumstances that require careful consideration in the current tax year. If you used a professional tax preparer previously, consider scheduling a brief consultation to discuss any significant changes in your financial landscape.

Verification is key to this process. Create a checklist that compares your current financial documents against the previous year’s return. Note any substantial differences in income, deductions, or credits. This comprehensive review not only ensures accuracy but also helps you anticipate potential tax implications for the current filing season. Your goal is to approach tax preparation with confidence, armed with a thorough understanding of your financial history.

Step 4: Consult with a Tax Professional or Accountant

Navigating the complex landscape of tax preparation often requires professional expertise. Consulting with a tax professional or accountant can transform your tax filing from a potentially stressful experience into a strategic financial planning opportunity. This step is particularly crucial for individuals with complex financial situations, significant life changes, or intricate income streams.

Begin by identifying the right type of tax professional for your specific needs. Certified Public Accountants (CPAs), enrolled agents, and tax attorneys each bring unique skills to the table. A CPA might be ideal for comprehensive financial planning, while an enrolled agent specializes exclusively in taxation. Consider your financial complexity and seek a professional whose expertise matches your requirements.

Prepare for your consultation by gathering all relevant financial documents. Create a comprehensive folder including:

- Previous years’ tax returns

- Current income statements

- Investment documentation

- Receipts for potential deductions

- Documentation of major life changes

Research potential tax professionals through professional networks, recommendations from trusted colleagues, and verified credentials. According to IRS guidelines, verify credentials and check for any disciplinary actions before making a final selection. Many professionals offer initial consultations, allowing you to assess their communication style and understanding of your unique financial situation.

During the consultation, be transparent about your financial circumstances. Discuss significant events from the past year such as marriage, divorce, job changes, property purchases, or investment activities. A skilled tax professional can identify potential tax strategies, uncover overlooked deductions, and provide guidance on future financial planning.

Verify the consultation’s effectiveness by assessing the professional’s proposed strategy. A successful meeting should provide clear insights into your tax situation, potential savings opportunities, and a structured approach to filing. Request a detailed summary of recommendations and discuss any questions or concerns thoroughly. Remember, the goal is not just to complete your tax return, but to optimize your overall financial health through informed tax planning.

Step 5: Prepare and File Your Tax Forms

Filing your tax return represents the culmination of your careful preparation. This critical step transforms your organized financial documents and strategic planning into an official submission to the tax authorities. Selecting the right filing method is crucial to ensuring a smooth and accurate tax submission process.

Electronic filing offers significant advantages over traditional paper submissions. Modern tax preparation software and online platforms provide user-friendly interfaces that guide you through complex tax forms step by step. These digital tools often include built-in error checks, automatically calculate potential deductions, and provide immediate confirmation of submission.

According to IRS e-file options, electronic filing is recommended for its speed, security, and reduced error rates. Choose a reputable tax preparation platform that matches your specific financial situation. Some popular options include commercial software like TurboTax and H&R Block, as well as free filing options for those with simpler tax returns.

Before final submission, conduct a comprehensive review of all entered information. Critical areas to double-check include:

- Personal information accuracy

- Social Security numbers

- Income reporting

- Deduction calculations

- Bank account details for refund or payment

Pay close attention to potential mathematical errors or discrepancies between your documentation and submitted forms. If you discover any mistakes, most electronic filing platforms allow you to make corrections before final submission. For more complex tax situations, consider having a tax professional review your completed return before filing.

After submission, save a complete copy of your tax return and all supporting documentation. Create both digital and physical backups, storing them in a secure location. Keep these records for at least three years, as the IRS may request additional information or conduct an audit. Confirmation of successful filing typically arrives via email or within the tax preparation platform, providing peace of mind that you have completed this critical financial responsibility.

Step 6: Verify Submission and Confirm Receipt

The final stage of tax preparation involves carefully verifying your submission and ensuring official receipt by tax authorities. This critical step provides peace of mind and protects you from potential filing complications. Your goal is to confirm that your tax return has been successfully processed and acknowledged.

Immediate after filing, carefully review the electronic confirmation or receipt provided by your tax preparation platform. Pay close attention to key details such as:

- Submission timestamp

- Confirmation number

- Processing status

- Expected refund amount (if applicable)

- Electronic or mailing address on file

According to IRS guidelines, most electronically filed returns are typically processed within 21 days. Create a dedicated tracking system to monitor your return’s status. Most tax preparation software and the official IRS website offer online tools that allow you to track your return’s progress in real-time.

For those who have filed a paper return, request a certified mail receipt that provides proof of submission. This documentation serves as critical evidence in case of any future disputes or processing delays. Keep all related correspondence and tracking information in a secure, easily accessible location.

Establish a follow-up schedule to track your return’s status. If you are expecting a refund, most electronic filing systems provide estimated deposit dates. Mark these dates on your calendar and set reminders to check the status if the anticipated refund does not arrive within the expected timeframe.

Should you discover any discrepancies or encounter processing issues, contact the relevant tax authority immediately. Have all your submission documentation readily available, including confirmation numbers, submission timestamps, and copies of your filed return. Prompt communication can help resolve potential problems quickly and efficiently, ensuring a smooth tax filing experience.

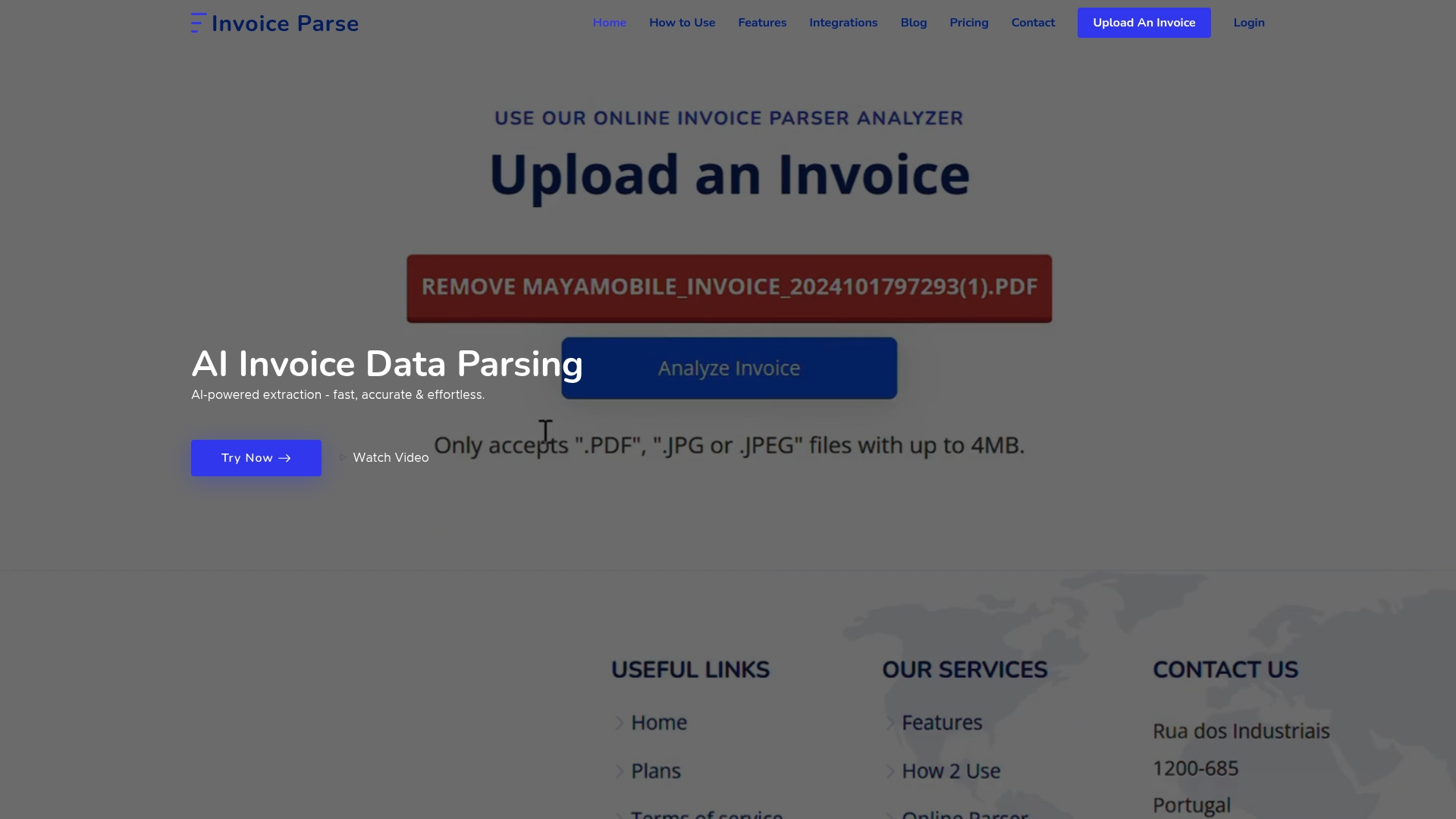

Stop Wasting Hours on Manual Invoice Sorting—Automate Your Document Organization Now

One of the biggest pain points highlighted in preparing for tax season is the overwhelming task of organizing and verifying stacks of financial paperwork like invoices and receipts. Missed or misfiled documents not only add to your stress but can also cause expensive errors during filing. If you have ever struggled to find critical vendor details or lost track of deductible expenses hidden in complicated PDF or image invoices, you are not alone. Fast, accurate data extraction and organization are not just helpful—they are essential for confidence and peace of mind during tax time.

Now is the perfect moment to make your tax prep smarter and headache-free. With Invoice Parse, you can instantly turn unstructured invoices into clean, searchable data, ready for Excel, Power BI, or your favorite workflow. Enjoy drag-and-drop uploads, seamless integrations, and powerful features like automated history and tagging, built for individuals and teams who must be audit-ready. Do not wait until your next audit or tax filing panic—discover how AI-powered invoice parsing can transform your tax season from chaos into clarity. Get started now with a free trial or subscription plan and take the stress out of financial documentation today.

Frequently Asked Questions

What are the first steps to prepare for tax season?

To prepare for tax season, start by organizing your financial documents such as W-2s, 1099s, and previous tax returns. Create a dedicated workspace and sort your documents chronologically and by type to ensure a smooth filing process.

How can I identify available tax deductions and credits for my tax return?

Examine your life circumstances for the past year, looking for events such as marriage, home purchase, or education expenses. Research applicable deductions like mortgage interest, education credits, and business-related expenses, and create a worksheet to document your findings.

Why is it important to review last year’s tax return before filing?

Reviewing last year’s tax return helps identify patterns and potential errors, ensuring a smoother preparation for the current tax season. It allows you to cross-reference income sources and check for any significant changes in your financial situation.

When should I consult a tax professional?

You should consult a tax professional if you have a complex financial situation, significant life changes, or if you are unsure about maximizing deductions and credits. A professional can provide personalized guidance and help navigate intricate tax rules.